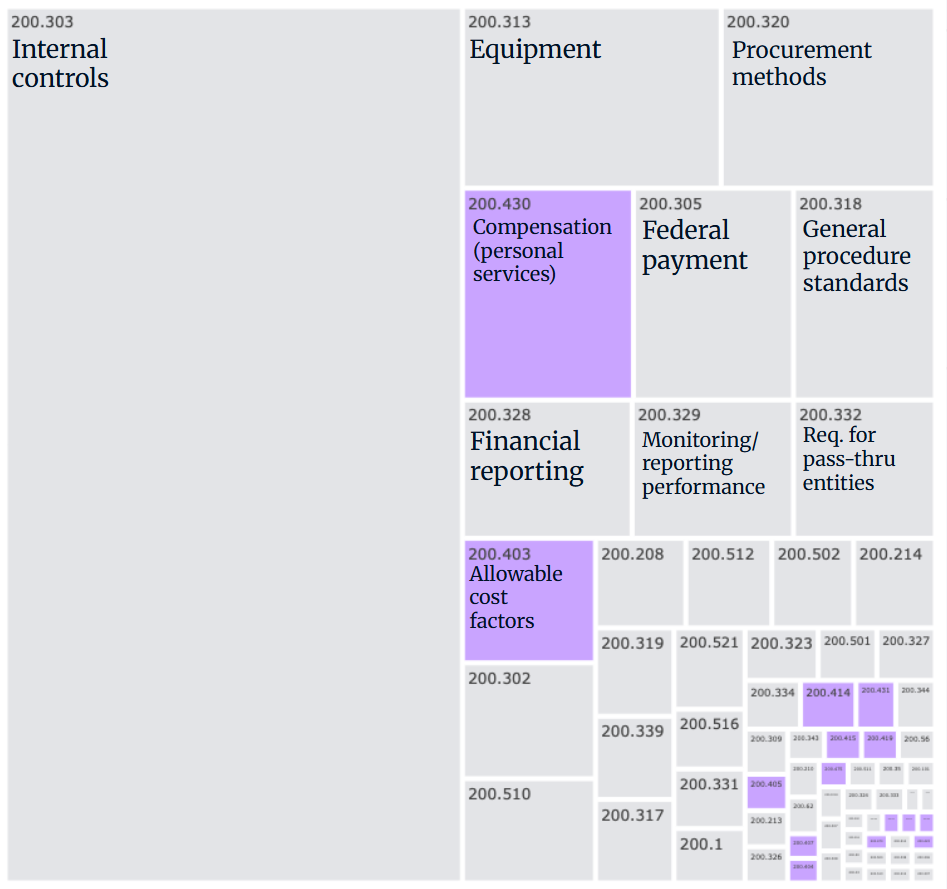

Regulatory citations in FAC findings

The plot summarizes audit findings by the regulation cited in each finding. The purple segments correspond to cost principles (allowability rules). They are a relatively small share of the total.

That distribution told us historical noncompliance is not dominated by narrow cost-allowability disputes. We deliberately expanded the product beyond transaction-only allowability inference into cash controls, grant context, and sponsor-specific risk.